EBITDA Multiples for Trucking Companies in 2026: What Your Business Is Actually Worth

EBITDA multiples for trucking companies in 2026 range from 3X for asset-heavy carriers to 8X or higher for asset-light logistics platforms — and the gap between those numbers represents millions of dollars at exit. If you have built a trucking company that moves freight, pays its drivers, and turns a profit, you need to know which end of that range you are on and exactly what is holding you back from the premium tier.

The answer comes down to EBITDA multiples — the earnings multiplier that determines your exit price. In the current trucking M&A market, that multiplier ranges from 3X at the low end to 8X or higher at the premium end, depending on five specific factors that most trucking owners have never had explained clearly.

This guide gives you the real picture: what trucking EBITDA multiples look like in 2026, what transaction data says buyers are actually paying, and the exact factors that move your business from the commodity end of the range to the premium end.

The Trucking M&A Market in 2026: What Is Actually Happening

The trucking and freight industry has been under significant consolidation pressure for several years — and that pressure directly shapes what EBITDA multiples for trucking companies look like today. High interest rates compressing freight rates, persistent driver shortages, and fuel cost volatility have created operating stress for smaller carriers — which simultaneously accelerates exit decisions and creates acquisition opportunities for well-capitalized buyers.

The result: strategic acquirers are the dominant buyers in 2026.

Larger carriers and third-party logistics providers are purchasing smaller operators specifically for lane density, driver capacity, equipment, and contracted shipper relationships. Private equity in essential services follows a different pattern — PE involvement in trucking varies sharply by sub-sector: asset-light freight brokerage and logistics technology companies attract far more PE interest — and far higher EBITDA multiples for trucking companies — than traditional asset-heavy carriers.

Active Acquirers in the Trucking and Logistics Space

- Knight-Swift Transportation — One of the largest carriers in North America, consistently acquiring regional operators for geographic density and driver capacity

- Heartland Express — Active acquirer of regional truckload carriers with a documented acquisition track record

- XPO Logistics — Strategic acquirer in LTL (less-than-truckload) and freight brokerage

- Echo Global Logistics / CEVA Logistics — Active in freight brokerage and 3PL consolidation

- Private equity in asset-light logistics — Firms including Francisco Partners and Warburg Pincus have been active specifically in asset-light freight brokerage and logistics technology, where multiples are significantly higher than asset-heavy trucking

Key insight: The buyers paying top-of-range multiples are not purely financial buyers. They are strategic operators seeking specific lane density, driver capacity, or technology capabilities they cannot build organically.

What EBITDA Multiples for Trucking Companies Actually Look Like

The honest answer: trucking EBITDA multiples vary more by business model than almost any other industry. The difference between asset-heavy truckload carriers and asset-light freight brokers is structural — and it produces dramatically different acquisition prices for businesses with similar revenue.

| Company Profile | Typical Multiple | Key Driver |

|---|---|---|

| Small asset-heavy carrier (under $5M revenue) | 2X–4X EBITDA | High equipment costs, driver dependency, thin margins |

| Mid-market truckload carrier | 3X–5X EBITDA | Lane density, driver base, equipment value |

| LTL carrier with strong regional density | 4X–6X EBITDA | Network density, recurring shipper relationships |

| Asset-light freight brokerage | 5X–8X EBITDA | Recurring shipper contracts, technology-enabled, scalable |

| 3PL / managed logistics provider | 6X–9X EBITDA | Technology platform, recurring revenue, asset-light scalability |

| Logistics technology / TMS platform | 8X–15X+ EBITDA | SaaS-structured recurring revenue, high margins |

How to Calculate Your Adjusted EBITDA

EBITDA = Earnings Before Interest, Taxes, Depreciation, and Amortization.

For acquisition purposes, buyers use Adjusted EBITDA — which adds back the owner’s personal compensation above a market-rate salary, one-time expenses, personal vehicles, and any non-recurring costs. This adjusted figure is what the multiple gets applied to.

Real-world example: A $5M revenue trucking company with $400K in net income may carry $700K–$900K in Adjusted EBITDA once personal compensation and non-recurring items are normalized.

- At 5X → that is a $3.5M–$4.5M business

- At 7X → that is a $4.9M–$6.3M business

Getting your EBITDA normalized before any buyer conversation is one of the highest-return preparation steps you can complete. A $400K swing in Adjusted EBITDA is worth $2M–$3.2M at a 5–8X multiple. If you operate in adjacent service verticals, the same logic applies — understanding what is my service business worth before entering any M&A process is foundational exit preparation regardless of industry.

Why Asset-Light Commands Premium Multiples

Asset-heavy trucking — owning a large fleet, employing drivers directly, maintaining equipment — creates structural valuation headwinds that depress multiples regardless of revenue.

The Asset-Heavy Problem

High capital requirements, driver turnover costs, maintenance unpredictability, and fuel exposure all suppress EBITDA margins and increase buyer risk. The average net margin for asset-heavy truckload carriers runs 3–6% in a healthy freight environment — and significantly lower during downturns like the 2023–2024 cycle.

Every dollar of equipment on your balance sheet represents:

- Capital the buyer must maintain, replace, or finance

- Risk that suppresses the return on their acquisition price

- A ceiling on how high your multiple can go

The Asset-Light Advantage

Asset-light freight brokers and 3PLs eliminate most of these headwinds. They match shippers with carriers, earn a margin on the spread, and scale revenue without proportional capital investment.

Buyers pay 5X–8X for asset-light logistics businesses because the model is:

- Capital-efficient (no fleet to maintain or replace)

- Scalable (revenue grows without proportional asset investment)

- Predictable (contracted recurring revenue from established shipper relationships)

These are precisely the characteristics that command premium acquisition multiples from both strategic buyers and private equity acquirers.

The Technology Factor: How Proprietary Intelligence Moves Trucking Multiples

The trucking industry is in the early stages of a technology-driven valuation bifurcation. Where your business lands on that divide is increasingly the single most important multiple driver in 2026.

Commodity Technology = No Multiple Advantage

Companies running generic Transportation Management Systems available to every competitor — McLeod, TMW, Samsara, KeepTruckin — derive zero valuation advantage from their technology investment. Buyers see commodity tools and price accordingly.

Proprietary Intelligence = Multiple Premium

Companies that have built Proprietary Intelligence — autonomous load matching and routing systems trained on years of their specific lane data, shipper behavior patterns, and carrier performance history — create genuine competitive moats that buyers recognize and pay premiums for.

A freight brokerage with a proprietary load optimization system that uses its accumulated transaction history to match loads faster and at better margins than competitors is not a commodity brokerage. It is a technology-enabled logistics platform. The acquisition multiple reflects that classification.

This is not theoretical. The acquisition of Echo Global Logistics by CEVA — representing a significant premium to book value — was explicitly driven by Echo’s technology platform and data assets, not just its freight volume. Buyers in logistics M&A are increasingly paying technology multiples for logistics businesses that have built genuine intelligence infrastructure.

The Five Factors That Determine Your Trucking Company’s EBITDA Multiple

Understanding EBITDA multiples for trucking companies requires more than reading a range — it requires knowing which variables move the needle for your specific operation. These are the five factors that buyers and private equity acquirers weight most heavily in 2026.

Factor 1: Asset Intensity — The Largest Single Multiple Driver

Every dollar of equipment on your balance sheet represents capital that a buyer must maintain, replace, or finance. Asset-heavy carriers trading at 3X–4X EBITDA are being priced partly on tangible asset value, not purely on earnings power.

The path to higher multiples: Transition revenue mix toward asset-light brokerage and managed logistics services that generate margin without proportional equipment investment — without eliminating the carrier operation that anchors your customer relationships.

Factor 2: Shipper Contract Quality and Recurring Revenue

Spot market freight revenue — loads sourced one at a time from load boards — is valued at a significant discount to contracted shipper relationships.

Buyers want to see:

- Formal shipper agreements with established rate schedules

- Volume commitments from top-tier customers

- Revenue concentration not overly dependent on any single shipper

A trucking company where 70%+ of revenue comes from contracted shippers commands meaningfully higher multiples than one dependent on daily spot market sourcing. This is the trucking equivalent of recurring maintenance contracts in roofing or HVAC — and buyers pay for it accordingly.

Factor 3: Driver Dependency and Retention Infrastructure

The American Trucking Associations projects the industry will need to hire over one million new drivers in the coming decade. Driver turnover at many carriers runs into the double digits annually — in some cases approaching 90–100% — creating significant operational and valuation risk.

Buyers specifically analyze driver retention during acquisition due diligence because high turnover represents:

- Recruitment and training cost

- Service quality instability

- Operational risk that impacts post-acquisition performance

Companies with documented driver retention programs, above-market compensation structures, and systematized onboarding infrastructure command premium multiples because they have solved the problem buyers fear most.

Factor 4: Technology and Proprietary Intelligence Ownership

As outlined above, the gap between commodity TMS users and Proprietary Intelligence owners is the fastest-growing valuation gap in trucking M&A.

Buyers are paying technology premiums for logistics businesses that own their intelligence:

- Route optimization systems trained on proprietary lane data

- Load matching AI that improves with every transaction

- Shipper behavior models that predict demand and proactively manage capacity

The businesses achieving 6X–9X in today’s trucking M&A market are the ones that have crossed from service provider to intelligence platform.

Factor 5: Geographic Lane Density vs. Fragmented Coverage

A trucking company with dominant market share on specific high-volume lanes — strong coverage, consistent volume, efficient equipment utilization — is more valuable than one with thin coverage across dozens of fragmented markets.

Strategic acquirers pay explicit premiums for lane density that complements their existing network. Knowing your specific lane profile and which acquirers would pay a strategic premium for your geographic position is a critical component of exit preparation.

How Proprietary Intelligence Transforms a Trucking Company’s Valuation

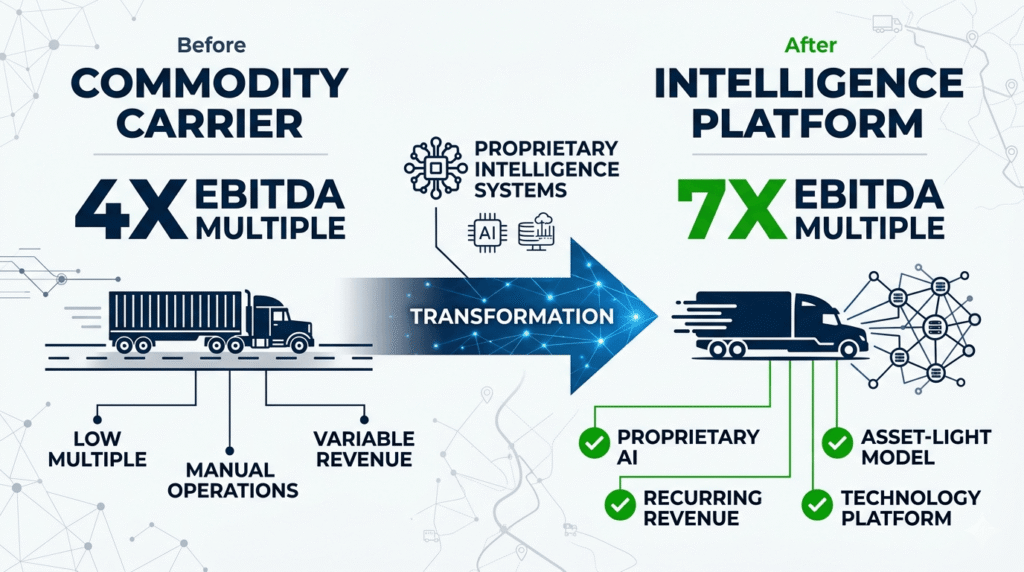

The path from a 3X–4X commodity carrier to a 6X–8X intelligence-enabled logistics platform follows a specific logic that Blue Dragon has applied across the logistics and transportation sector.

Three Intelligence Systems That Redefine Buyer Classification

1. Autonomous Load Optimization A load optimization intelligence system trained on years of your specific lane data, carrier performance history, and shipper demand patterns creates genuine competitive moat. It gets smarter with every transaction and produces load matching decisions that a competitor starting from scratch cannot replicate.

2. Shipper Intelligence Platform A platform that tracks shipper behavior, forecasts volume fluctuations, and proactively manages capacity allocation creates the recurring relationship infrastructure that commands recurring revenue multiples. Buyers pay more for businesses where the shipper relationship is embedded in a system, not just in a salesperson’s phone.

3. Driver Performance Intelligence A system that predicts turnover risk, optimizes route assignments, and systematizes the institutional knowledge currently living in your dispatcher’s head reduces the key-man risk buyers price into every acquisition.

The Buyer Classification Shift

Collectively, these systems transform how buyers classify your business:

Not a carrier with trucks. A logistics intelligence platform with a carrier operation attached.

That classification difference — carrier vs. platform — is worth millions at exit. The multiple expansion from 4X to 7X on $800K of Adjusted EBITDA represents $2.4M in additional exit value. On $1.5M of Adjusted EBITDA, that same shift represents $4.5M.

The Blue Dragon Guarantee

If Blue Dragon cannot demonstrate a clear, documented path to at least doubling your current business valuation through Proprietary Intelligence, we issue a complete full refund. No questions. No conditions. No fine print.

We are one of the only firms in this space that makes this commitment.

Frequently Asked Questions

What EBITDA multiple can I expect for my trucking company in 2026?

EBITDA multiples for trucking companies in 2026 range widely depending on business model and the five factors outlined above. Asset-heavy truckload carriers typically trade at 3X–5X EBITDA. Asset-light freight brokers and 3PLs command 5X–8X. Logistics technology and TMS platforms with recurring revenue can reach 8X–15X+.

The specific multiple for your business depends on asset intensity, shipper contract quality, driver retention infrastructure, technology ownership, and geographic lane density. Blue Dragon’s Valuation Audit produces a pre- and post-intelligence multiple model specific to your operation.

Why do asset-light logistics companies get higher EBITDA multiples than carriers?

Asset-light businesses are more capital-efficient, more scalable, and produce more predictable margins — all characteristics that buyers and private equity acquirers pay premiums for. Asset-heavy carriers require ongoing equipment investment, face fuel and maintenance volatility, and carry driver turnover risk.

Every additional dollar of assets on the balance sheet represents risk and capital requirement that suppresses the return a buyer can earn on their acquisition price. The path to higher multiples is transitioning toward asset-light revenue — brokerage, managed logistics, technology services — without eliminating the carrier operation that anchors customer relationships.

Does my trucking company need to be asset-light to get a premium multiple?

The freight market has been in a prolonged down cycle since late 2022, with spot rates compressed and carrier profitability under pressure. This creates a valuation paradox: depressed EBITDA makes multiples appear lower in absolute dollar terms.

However, well-run carriers with strong contracted shipper relationships and Proprietary Intelligence infrastructure are distinguishing themselves from the commodity market and attracting strategic acquirer interest even in a difficult freight environment. The most active buyers in trucking M&A in 2025–2026 are strategic operators seeking specific lane density or technology capabilities — not purely financial buyers chasing earnings.

Does my trucking company need to be asset-light to get a premium multiple?

Not necessarily — but asset intensity significantly shapes your valuation ceiling. Asset-heavy carriers can achieve premium multiples within their category by demonstrating:

– Strong contracted shipper relationships (recurring revenue)

– Documented driver retention infrastructure

– Technology-enabled dispatch and routing

– Geographic lane density that strategic acquirers cannot build organically

The goal is not to eliminate assets but to ensure the business generates recurring, predictable revenue from those assets rather than commodity spot market volume.

What is the impact of AI and automation on trucking company valuations?

Significant and growing. Buyers in 2025–2026 specifically evaluate whether a logistics business has technology that creates genuine competitive advantage or just operational efficiency. Generic TMS software creates no valuation advantage.

Proprietary load optimization systems trained on your specific lane data, autonomous dispatch intelligence, and shipper behavior AI create competitive moats that buyers pay premiums for. The trucking businesses commanding 6X–8X today are the ones that have built intelligence infrastructure competitors cannot fast-follow.

What is Blue Dragon’s guarantee for trucking and logistics businesses?

If Blue Dragon cannot demonstrate a clear, documented path to at least doubling your current business valuation through Proprietary Intelligence, we issue a complete full refund. No conditions. No fine print.

We are one of the only firms in this space that makes this commitment.

Related Valuation Guides

These sector-specific guides follow the same EBITDA multiple framework applied in this article. If you operate in or are advising businesses across adjacent trades and service verticals, these are the reference points buyers are using:

- EBITDA multiple for construction companies — How construction firm valuations compare to trucking, and the factors that move multiples in a capital-intensive trade business

- Sell my plumbing company — What plumbing business owners need to know before entering the M&A market, and how to position for a premium exit

- Sell my fire protection company — Valuation benchmarks and buyer landscape for fire protection businesses in 2026